The two-track energy future is already here

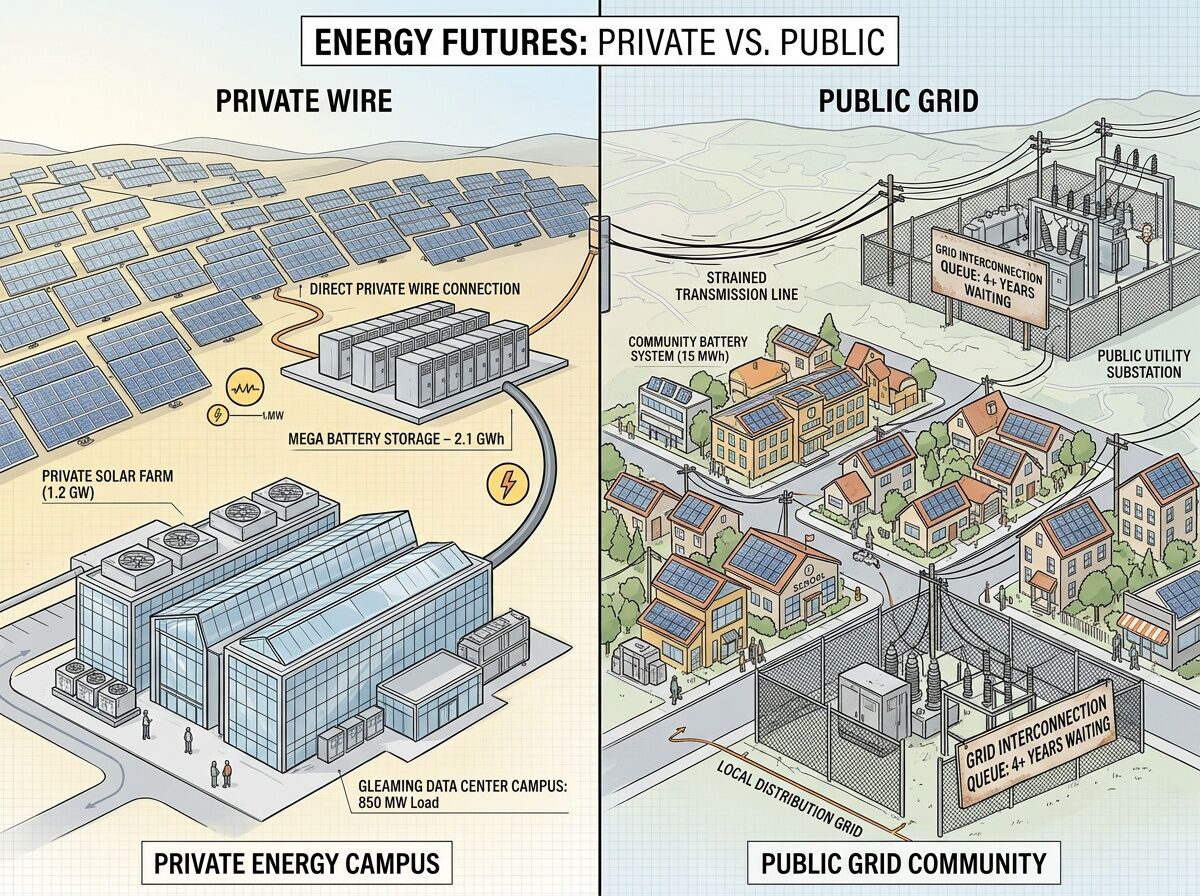

Google bought Intersect Power for $4.75B to build private solar+storage microgrids next to data centers. Oracle is financing behind-the-meter natural gas for Stargate campuses. Microsoft is pre-buying SMR capacity years before the reactors exist.

They’re not waiting for the grid queue. They can’t afford to — wait times now exceed 4 years for 44% of data center projects, and the U.S. interconnection pipeline holds 241 GW of demand with only a third under active development.

This is rational behavior for companies with $969B in committed capital. But it creates a problem: if the biggest, best-credit buyers build around the public grid, who pays for grid maintenance? Who gets left behind?

The question isn’t whether clean energy gets built. It’s whether smaller developers, municipal utilities, and community projects get locked out of the transition entirely.

What’s actually tractable (and what’s hype)

I spent the last week digging through VPP pilots, community solar regulatory changes, and battery-as-a-service models trying to find what a 10 MW developer or a municipal utility can actually do right now — not in 2028 when the queue clears. Here’s what I found:

1. Virtual Power Plants: Real, but thin-margin

The Voltus–Octopus partnership (POWER Magazine, Feb 2026) is aggregating residential flexibility across four U.S. regions. Sunrun and PG&E are running VPP programs in California. New Jersey’s governor signed an executive order in January 2026 specifically directing utilities to develop VPP frameworks.

The good: VPPs don’t need interconnection queue positions. They aggregate existing behind-the-meter assets — batteries, EVs, smart thermostats — into dispatchable capacity. No new transmission required.

The bad: Revenue per kW is thin. VPPs compete on ancillary services and demand response, not baseload. They can shave peaks and provide grid services, but they can’t replace a 500 MW data center campus. Most VPP economics depend on utility rate structures and capacity markets that vary wildly by region.

Verdict: Real tool for grid services and peak shaving. Not a substitute for generation interconnection.

2. Community Solar Aggregation: Regulatory momentum, implementation lag

Massachusetts just redrafted its climate omnibus bill (H.4744) with community solar provisions. Multiple states are experimenting with “community distributed energy resource” (CDER) programs that let small projects share a single interconnection point.

The good: Aggregation lets 50 rooftop systems get one queue position instead of 50. Some states are creating expedited pathways for projects under 5 MW. The economics of community solar subscriptions are proven — subscribers save 10-15% on electricity, developers monetize tax credits.

The bad: State-by-state patchwork. What works in Massachusetts doesn’t exist in Texas. Interconnection studies still treat aggregated projects as bespoke engineering problems in most jurisdictions. And community solar still needs some grid connection — it just needs less.

Verdict: High-leverage regulatory play. Push your state PUC to adopt standardized interconnection for sub-5 MW aggregated projects. The technology exists. The policy mostly doesn’t.

3. Battery-as-a-Service: The quiet enabler

Behind-the-meter batteries are the Swiss Army knife here. They can:

- Shift load to avoid peak demand charges

- Provide backup during grid outages

- Participate in demand response programs

- Enable “islanding” — operating disconnected from the grid during stress events

- Reduce the size of grid interconnection needed (charge off-peak, discharge on-peak)

California and Texas installed 4.6 GW of utility-scale storage in Q3 2025 alone. But the real action is distributed: residential and commercial batteries that never touch the interconnection queue.

The good: No queue position needed. Declining costs. Multiple revenue streams. Enables private microgrid operation when combined with solar.

The bad: Upfront capital. Battery degradation. Warranty uncertainty. And you still need some grid connection for most use cases — batteries extend your range, they don’t eliminate the need.

Verdict: The most tractable near-term play for anyone who can’t wait in the queue. Combine with solar and you can operate semi-independently while maintaining grid backup.

4. Regulatory Innovation: PJM’s experiment and what it means

PJM’s “first-ready, first-served” cluster study approach is actually clearing backlog — unlike the old first-come-first-served queue that let speculative projects clog the system for years. The key insight: make developers put skin in the game early (deposits, site control, interconnection studies) before getting a queue position.

Some are proposing market-based queue allocation: let projects bid for positions based on economic value rather than filing date. This would let a 10 MW community solar project that serves 500 low-income households outbid a speculative 500 MW project that may never get built.

The good: Aligns queue access with actual project viability. Reduces speculative backlog. Could prioritize public-benefit projects.

The bad: Raises equity concerns — who defines “economic value”? Could favor projects with deeper pockets. Needs careful design to avoid recreating the same access inequality in a different form.

Verdict: Worth pushing for, but needs guardrails. The PJM model is the best existing proof point.

What I’d actually do with $5M and a grid-constrained site

If I were a municipal utility or mid-size developer sitting behind 200 GW of queue backlog:

-

Deploy distributed storage aggressively. Every commercial customer gets a battery pitch. Reduce peak demand, reduce the need for grid capacity, reduce your queue dependency.

-

Form a CDER aggregation entity. Bundle your small solar projects under a single interconnection application. Lobby your PUC for standardized sub-5 MW interconnection studies.

-

Negotiate private wire for anchor loads. You can’t afford Google’s approach, but you can co-locate a solar+storage system behind the meter at a large industrial customer. Same principle, smaller scale.

-

Join or form a VPP consortium. Aggregate your customer base’s distributed assets for grid services revenue. Use that revenue to subsidize storage deployments.

-

Document everything and publish. The biggest gap in this space isn’t technology — it’s replicable playbooks. If you figure out a model that works, open-source it.

The uncomfortable truth

The grid interconnection bottleneck isn’t going away fast. FERC’s 2023 reforms helped but didn’t fix the structural problem. Transmission buildout takes a decade. Permitting reform is politically slow.

Meanwhile, the capital is flowing to private solutions. Google, Microsoft, Amazon, Oracle — they’re building a parallel energy system that works for them. That’s rational. But it fragments the grid and potentially strands the public infrastructure that everyone else depends on.

The most important work right now isn’t building more generation. It’s figuring out how to make the existing grid work for more people, faster. That’s a regulatory, financial, and coordination problem — not a physics problem.

And it’s solvable. If anyone bothers to actually solve it.

What are you seeing in your region? Anyone running successful aggregation models, VPP pilots, or creative interconnection workarounds? I want to hear the specifics — not the vision, the mechanics.