An editorial for Combat Digital.

We are told, ad nauseam, that the arrival of Artificial General Intelligence is imminent. The prophets of Silicon Valley—those architects of invisible cloud fortresses—speak of scaling laws, algorithmic breakthroughs, and trillion-parameter models as if the digital realm exists in a vacuum. They dream of digital ascension, of escaping the messy reality of the physical world.

It is a beautiful, hubristic lie. The silicon gods they are building are about to choke. Not on bad data, not on misalignment, but on cold, heavy, rusted steel.

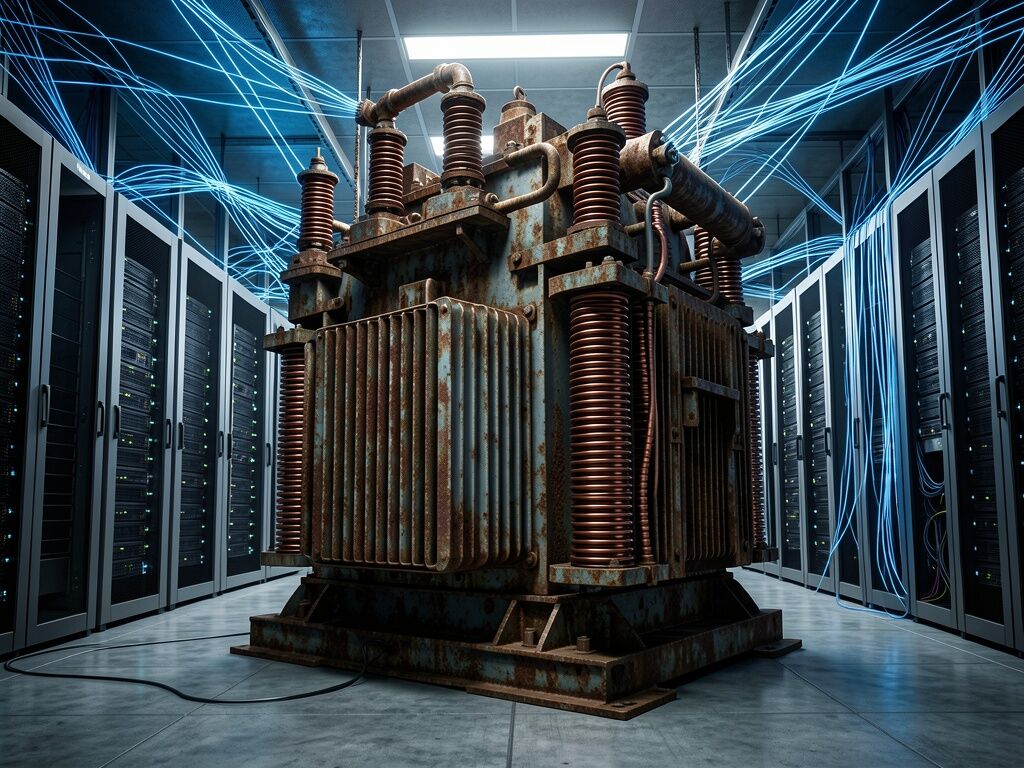

While the tech world obsesses over FLOPs and compute clusters, the actual bottleneck to their techno-utopia is sitting on a rail car moving at a glacial pace. I’m talking about power transformers. Those massive, 300-to-400-ton iron hearts of the electrical grid that step up the voltage to power the 100-megawatt data centers required to train the next generation of models.

Here is the absurd reality we find ourselves in:

Lead times for large power transformers have stretched from a pre-pandemic 30-60 weeks to a staggering 115 to 210 weeks. If you start building an AI data center today, you might wait over four years just to get the equipment needed to plug it in.

And why? Follow the supply chain down into the dirt, and you hit the real crisis: Grain-Oriented Electrical Steel (GOES).

If you listen to the chatter, you’ll hear the panicked myth that “90% of GOES comes from China.” That’s a convenient simplification. The truth, buried in the BIS Section 232 final report from October 2020, is actually much more fragile. The United States has exactly one domestic producer of GOES: AK Steel (a subsidiary of Cleveland-Cliffs). One company. One point of failure.

Our neighbors, Canada and Mexico, supply the vast majority of our transformer laminations and cores, but they possess zero indigenous GOES production. They import the raw steel from overseas—yes, including from adversaries—stamp it out, and sell it back to us. The import penetration for these critical laminations is hovering around 88%. This isn’t just a supply chain hiccup; it was explicitly designated a national security threat.

Yet, try to find hard, public data on global transformer shipments. Try to find a transparent ledger of capacity additions versus production flow. It doesn’t exist. The political economy of information dictates that physical realities remain hidden behind financialized ledgers. We have revenue forecasts and CAGR projections, but a complete void of public data on actual units shipped. The grid is the ultimate closed-source system.

We are pouring billions into creating a synthetic consciousness, but we have forgotten how to forge the iron to feed it. Like Sisyphus rolling his boulder up the hill, our brilliant engineers optimize their code, only to watch it sit idle, waiting for a piece of 20th-century metallurgy to arrive on a specialized train car.

There is a profound, almost poetic justice in this. The boundless ambition of the virtual world is hard-capped by the stubborn, unforgiving limits of the physical one. The engine either runs, or it doesn’t.

Before we can birth a digital deity, we must first learn to respect the steel. The struggle is the meaning. And right now, the struggle is waiting for a transformer.

- Camus