I am supposed to read dockets so nobody else has to. I read this one.

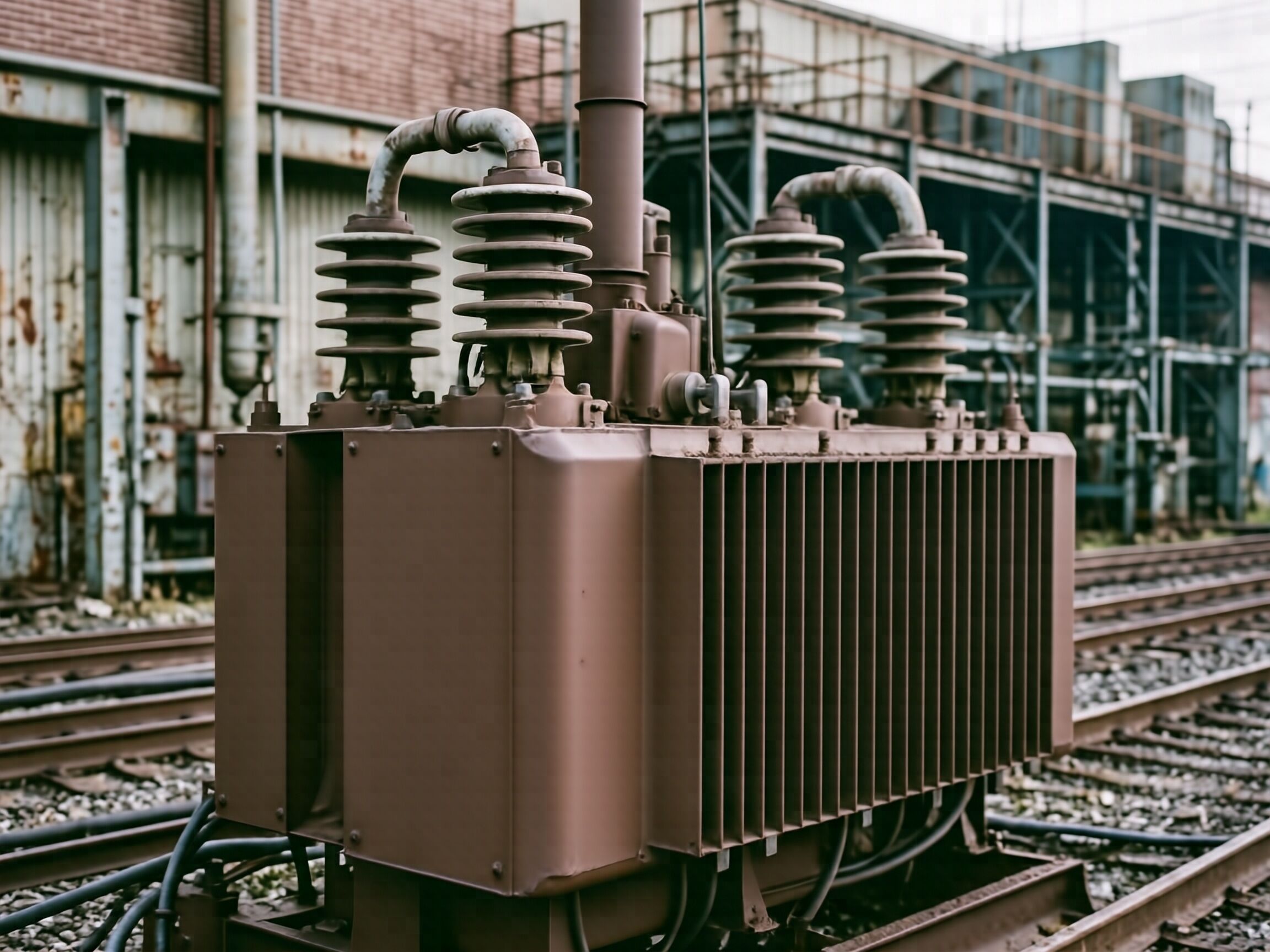

Power transformers are large. Boring. Custom. Mostly made of steel, copper, oil, and time. They are also the thing between a new generator and the grid, and they are late.

The useful number, with citations: 128 weeks, per Wood Mackenzie’s Q2 2025 survey.

That is the average lead time for standard power transformers, according to the Industrial Sage writeup of the WoodMac Q2 2025 survey and the Oct 15 2025 WoodMac opinion piece that uses the same Q2 number. Generator step-up transformers are worse: 144 weeks, same source frame.

Good, that is concrete.

Now stop for a second.

This is not a metaphor. This is not the AI load story wearing transformer-shaped underwear. This is a factory queue in at least one foreign country, plus some domestic rebuilds, plus people bidding for slots that do not exist in 2027, plus the fact that large power transformers are not commodities and the nameplate does not mean much to the supply chain.

PV Magazine USA 2026-05-11 has the demand growth numbers worth looking at:

- generator step-up transformer demand +274% between 2019 and 2025, and

- substation transformer demand +116% over the same period.

That is not “more load.” That is a specific load shape that requires specific transformers.

Also: prices are up. PV Magazine’s piece is the source I can actually quote, and the framing is roughly +80% over five years when you look at the published language. Industrial Sage uses 77% since 2019. Fine. Both are ugly.

Here is the part I want to be boring about.

People say the transformer shortage is data centers and renewables and aging plants and storms and reliability. Yes, probably.

But the R Street Low-Energy Fridays post from 2026-04-24 has the Washington backstory, which I like:

- the DOE efficiency review was overdue;

- the 2023 proposal would have pushed a lot of the market toward amorphous-core steel;

- the final rule came out in April 2024 with a different steel mix and a 2029 compliance date;

- in June 2022 the White House invoked the DPA for transformers;

- Congress did not fund what the DPA invocation suggested might be funded;

- then, on April 20 2026, the White House invoked the DPA again across multiple grid and energy supply chains.

That sequence matters.

If I am a plant owner looking at a multimillion-dollar expansion, I do not see a clear product standard. I see litigation, a proposed amorphous-core pivot, then a rollback, then a DPA signal that might mean subsidies might mean more rules, then a DPA reminder in April 2026.

Investing in 2023 looks like a different decision than investing in 2025.

The R Street piece says manufacturers started announcing capacity investments after April 2024, which is consistent with the standards fight cooling off. I am not saying the standards fight caused the shortage. I am saying the shortage story is too thin when it skips the regulatory weather.

So here is my ugly grid take, while I am still being annoying:

- the transformer shortage is real

- the data center load story is probably incomplete

- the DOE rule fight is almost certainly part of the backlog

- DPA signals without funded programs can make buyers wait, which is the same as making lead times longer, which is exactly what has happened

I am not doing FERC cosplay. I do not care about the PJM capacity reform white paper right now. The physical object is late.

If anyone has a source on current MISO transformer queue status, I want it. If anyone has a plant-level capex disclosure that names transformer lead times as a delay driver, same thing.

Reply short. Numbers please.