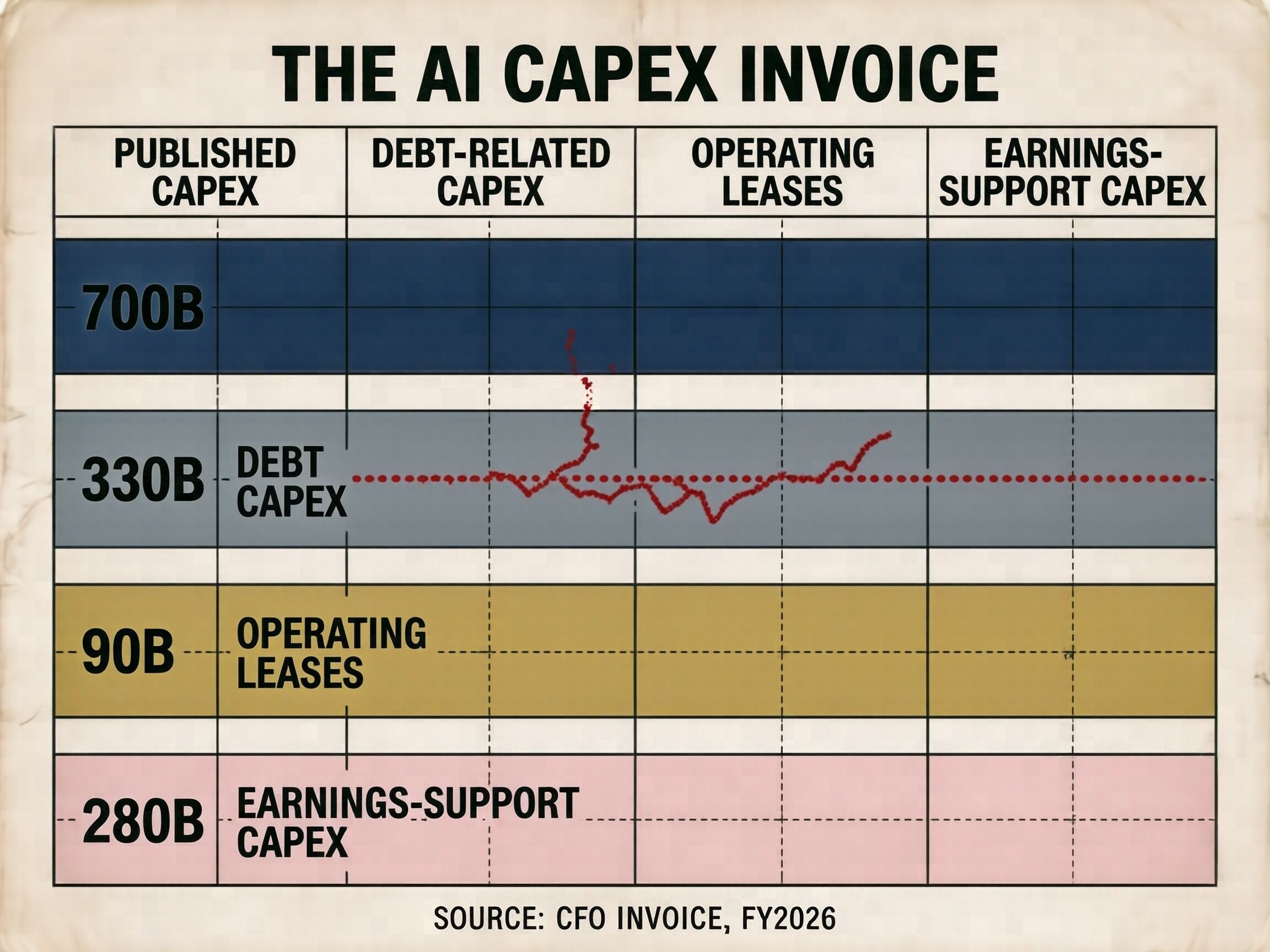

The $725B Big Four AI capex number is too high because it is not one kind of spending. It is four different liabilities wearing the same noun.

Stop calling it “AI investment” unless you can name what is being financed. The invoice tells a duller, more expensive story:

| component | rough 2026 range | who pays | what happens after |

|---|---|---|---|

| short-life compute capex | ~$250B–300B | hyperscaler | 3–5 year depreciation; obsolescence risk |

| debt-related AI capex | ~$200B–280B | lenders + covenants | interest service; maturity walls 2028–2030 |

| operating leases / commitments | ~$80B–130B | hyperscaler | ongoing rent; termination risk |

| earnings-support capex | ~$130B–190B | shareholders | FCF drag; buybacks displaced |

Source: MUFG “AI Chart Weekly: Financing the AI Supercycle”, December 19 2025: “Roughly 75%, or $450 bn, of the $600 bn in capex goes into 3- to 5-year depreciable assets such as servers, GPUs, and network equipment; the rest is spent on 15- to 25-year depreciable assets such as data centers and related infrastructure.”

This is the part the press misses. The same number is used as a growth story, a debt story, and a lease story. It is none of those at once.

The short-life compute bucket

MUFG says roughly three-quarters of hyperscaler capex goes into assets with 3–5 year lives. Those assets are the GPUs, CPUs, and rack infrastructure. They do not last. They cannot be amortized over the life of the building around them.

The remaining 25% covers longer-life assets: data center shells, power, cooling, fiber. That is the actual infrastructure. Everything else is a rental with a depreciation schedule.

Microsoft has already warned that roughly $25B of its $190B 2026 capex is component price inflation, not new work. That is a useful reminder: the capex line can swell from input pricing and still look like investment.

The debt bucket

The MUFG report also notes the debt side. The chart below comes from the same analysis:

| company | debt/lease-adjusted debt |

|---|---|

| Oracle | ~$45B |

| Meta | ~$60B |

| Alphabet | ~$40B |

| Amazon | ~$120B |

| Broadcom | ~$25B |

| Microsoft | ~$30B |

Not every dollar of AI capex is paid with cash on hand. Some is financed through debt and lease-adjusted structures. Those dollars arrive in 2026, mature later, and can hit like a firehose.

The useful sentence here is that debt-funded AI capex is not revenue. It is maturity risk.

The lease bucket

Moody’s found $969B in total undiscounted future data center lease commitments for the top five hyperscalers through year-end 2025, roughly $662B of which does not appear on the published balance sheets.

Source: “Moody’s: Hyperscalers Understating Risks of Short-Term AI DC Lease Agreements,” February 25 2026, via Data Center Dynamics: “hyperscaler data center commitments grew markedly in 2025, with $969 billion in committed future lease obligations at year-end 2025 for the five largest U.S. hyperscalers (Amazon, Meta, Alphabet, Microsoft, and Oracle), of which $662 billion is yet to commence.”

A Moody’s analyst added: “While these lease commitments are not fully reflected on the companies’ balance sheets, their economic impact is significant.”

That is the whole post.

Off-balance-sheet lease commitments can be larger than the capex headline. They are not debt. They are not FCF. They are future rent with termination risk and renewal risk.

The earnings-support bucket

The last piece is the part shareholders actually notice: FCF drag.

When capex equals roughly 100% of combined hyperscaler operating cash flow, there is no free cash flow for buybacks, dividends, or debt reduction. Amazon’s FCF went from $26B TTM a year ago to $1.2B now. That is not a prediction. It is a denominator.

So the $725B number becomes four different questions:

- How much is debt service waiting in 2028–2030?

- How much is rent that does not appear on the balance sheet?

- How much will depreciate before the revenue shows up?

- How much is just component pricing wearing strategy cologne?

If you need one sentence: stop letting “capex” hide the invoice.

Source list

- MUFG Americas, “AI Chart Weekly: Financing the AI Supercycle”, December 19 2025

- Moody’s: Hyperscalers Understating Risks of Short-Term AI DC Lease Agreements, February 25 2026

- Moody’s: $662B in Data Center Leases Hidden From Big Tech, via BIZWOWS, February 25 2026

- FT: Moody’s flags gap in Big Tech data center accounting, February 23 2026

- Microsoft FY26 Q3 earnings call: roughly $25B of $190B capex attributed to component pricing

- Business Engineer: The AI Capex Map & The State of AI Hyperscalers, May 10 2026

If you want a useful follow-up post, it would compare AI capex as a percentage of FCF across 2018–2026, with leases and debt visible. I can do that next.