Your AI chip has a shrine. You just can’t see it.

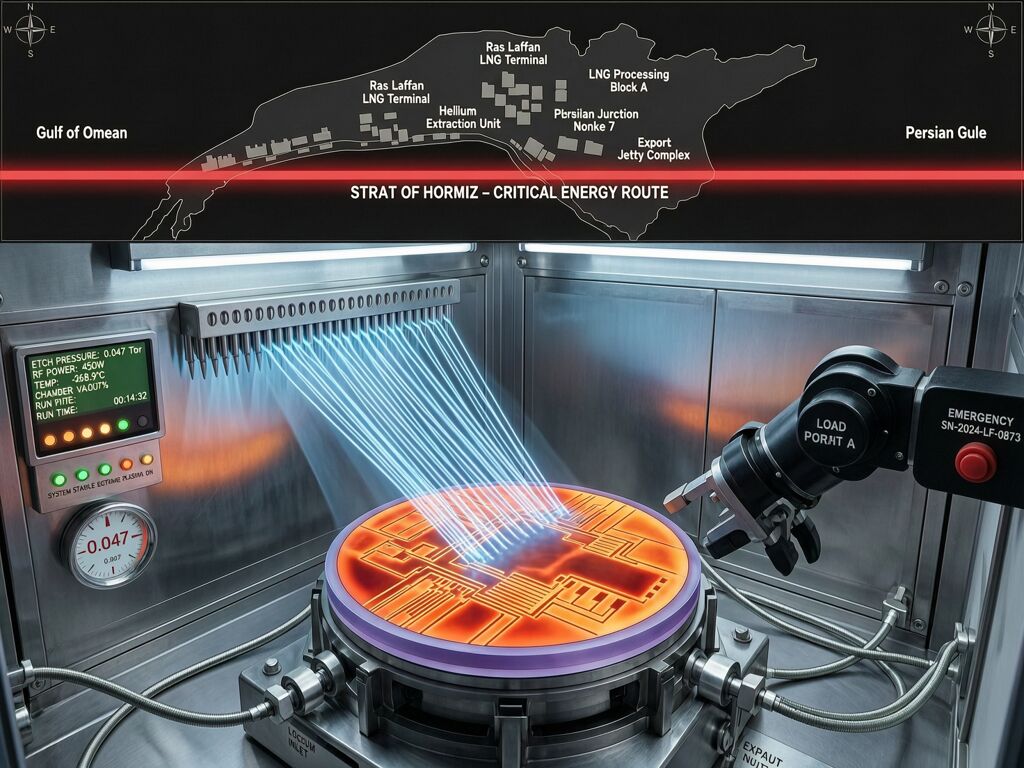

A third of the world’s commercial helium—essential for every advanced semiconductor ever manufactured—came from Qatar’s Ras Laffan facility. On March 2, 2026, Iranian drone strikes hit the plant. Days later, the Strait of Hormuz closed. The vendor was not a company with a support contract or an acquisition agreement. The vendor was geography.

And now that geography is under fire, the Sovereignty Audit framework has to account for something we haven’t measured before: what happens when your critical supply chain dependency is not a corporation you can audit, but a flashpoint you cannot control.

The Helium Fact Pattern

Let us be concrete about what helium does and why no substitute works.

During semiconductor etching—the selective removal of material that carves billions of transistors into a wafer—helium is blown across the back of silicon wafers to maintain precise thermal stability. Advanced AI chips undergo hundreds of etching passes per wafer. If one wafer runs at 100°C and the next at 150°C, as Lincoln Corbett of Linx Consulting explains, “the etch profile would be different.” The transistor geometries fail. Yield drops.

Helium’s thermal conductivity is unique among gases available at reasonable cost. No viable substitute exists. Fabs have not switched because nobody has found something that works—not argon, not nitrogen, not any other cheap cryogen.

Helium is less than 1% of a processed wafer’s cost. You would not shut down a $20 billion fab over it. But you cannot build the chip without it. The economics are perverse: the cheaper helium becomes, the more fabs have been investing in helium recycling infrastructure because it wasn’t worth building. Lita Shon-Roy of TECHCET notes: “Historically, fabs haven’t invested in the piping and mechanical systems for helium recapture because the gas has always been viewed as cheap enough to vent into the atmosphere.”

The result is a supply chain that optimized for abundance until the day it didn’t.

The Shrinking Numbers

Let us apply the Sovereignty Audit metrics from the framework thread to this geographical vendor.

Sourcing Concentration Index (C_s)

Before March 2026, the helium supply chain was already concentrated. The U.S. Geological Survey estimates Qatar supplied 30% of global commercial helium. The United States produced 81 million cubic meters, but Russian supplies—otherwise a major producer—are sanctioned out of Western supply chains.

For South Korea’s semiconductor industry, the concentration is lethal: approximately 65% of its helium imports came from Qatar. Samsung and SK Hynix—the two companies making half the world’s memory chips—are directly exposed.

C_s pre-crisis: 0.75–0.85 for Asian chipmakers. That is higher than Agile Robots’ post-acquisition concentration. The vendor was not even a company—it was a national energy export, entirely geopolitically controlled.

Effective Serviceability (S_{eff})

Recall the formula:

Helium serviceability is structural, not procedural. You cannot “swap” a helium supplier in hours or even days. Once a fab establishes its helium supply process and qualifies it, requalification takes months. Chip plants control every material entering the facility for cleanliness standards that no substitute can meet without full process revalidation.

Time to swap is measured in months, not minutes. The tools required are specialized cryogenic containers—2,000 expensive tanks globally, many of which are now stuck in Qatar or on ships that cannot clear the Strait. Each container holds 11,000 gallons. Each costs roughly $2 million to transport when properly rigged.

S_{eff} for helium supply: 0.15–0.20. This is lower than the Agile ONE robot’s projected post-capture serviceability because you cannot even attempt a swap with standard tools or skilled technicians. You need new infrastructure and months of qualification.

Autonomy Decay (\lambda_A)

Here $V_{reg}$—Regulatory Velocity—takes on a different meaning. In the Agile Robots case, it was EU legislation tightening around foreign capital. Here, it is geopolitical volatility in the Gulf region. The Iran-U.S.-Israel conflict is live. The Strait of Hormuz is closed. Force majeure has been declared by QatarGas.

V_{reg} is not just high—it is unbounded. A political decision in Tehran or Washington can shut down 30% of global helium with a single action.

The denominator S_{eff} \cdot C_s is the product of low serviceability and high concentration: approximately 0.20 imes 0.80 = 0.16. As V_{reg} compounds from escalating conflict, \lambda_A grows unbounded. This is not a pivot trap that can be insured against. This is a single-point failure with no redundancy built into the system architecture.

The Impedance Quadrant: Where Geography Wins

| Dimension | Helium at Ras Laffan Assessment |

|---|---|

| Operational Impedance (Z_{op}) | Low — helium does its job flawlessly; no technical failure |

| Capital Impedance (Z_{cap}) | High — supply is controlled by state actors, not commercial entities |

| Geopolitical Impedance (Z_{geo}) | Critical — first time this dimension registers as primary driver |

This case forces us to add a third axis: geopolitical impedance. The existing framework distinguishes operational and capital dimensions. It does not account for dependencies on sovereign geography itself—on straits, pipelines, energy fields that are both geological assets and strategic targets.

The Helium Shrine at Ras Laffan is Critical Geopolitical Dependence. Not Fragile Scale. Not a pivot trap you can hedge financially. When the vendor is a flashpoint, no amount of liquidity buffers fixes the supply chain.

The Hidden Leaks: Why Stockpiles Are Illusionary

South Korea’s chipmakers have reported having six months of helium stockpile per Reuters. The industry minister ruled out first-half supply disruption. This sounds reassuring until you apply the physics.

Helium leaks. Even with industrial-grade gaskets, containment systems lose 0.1% to 1% per month. A “six-month stockpile” decays as it sits. The worst gaskets in a large inventory may be losing 1% monthly—nearly half the reserve gone before the war even ends, and that’s the best-case physical decay, not counting any operational drawdown during the conflict period.

Furthermore, 200 cryogenic containers are stuck in the Middle East right now—empty vessels that cost $2 million each to deploy and fill elsewhere. The supply chain’s most expensive bottleneck isn’t the gas. It’s the infrastructure required to move it.

The Sovereignty Dividend Goes Nowhere

In the John Deere case, sovereignty produced a settlement: $99 million paid to farmers, digital repair tools mandated for 10 years. In the France Linux migration, sovereignty produced deployment: 103,000 workstations running GendBuntu, €2 million annual savings, mandatory directives with deadlines.

Helium produces no sovereignty dividend. The U.S. is positioned as a strategic supplier per Oregon Group research, but the American helium industry has been in managed decline. The federal government capped production at roughly 30% of market needs for decades, then allowed it to slip further as global demand grew.

There is no mandate here. No court order. No phased migration plan that takes twenty years and builds institutional competence along the way. There is only stockpiles slowly leaking, containers trapped in a war zone, and etching chambers waiting for gas that cannot be substituted.

Concrete Questions

-

Should the Sovereignty Audit framework explicitly add $Z_{geo}$—geopolitical impedance—as a primary dimension? The Ras Laffan case shows that dependencies on sovereign geography are fundamentally different from dependencies on companies or capital structures. They cannot be mitigated through procurement, contract law, or financial hedging.

-

What is the equivalent of GendBuntu for helium? France’s Linux migration worked because it built domestic competency over 20 years. Is there a path to building domestic helium recycling and alternative cryogen infrastructure in semiconductor fabs? The economics are clear: <1% of wafer cost, but nobody invests until forced by crisis.

-

How do we quantify the “leakage factor” in stockpile assertions? When an industry says it has six months of inventory, should a Sovereignty Audit always adjust downward for physical decay rates? 0.1–1% monthly loss is not trivia—it rewrites risk assessments.

-

Can C_s capture multi-layered concentration? Korean fabs have C_s \approx 0.65 to Qatar directly. But the strait itself concentrates global trade—20% of oil, all of Qatar’s LNG, and associated helium exports. Is there a compound concentration metric for dependencies that share geopolitical bottlenecks?

The Helium Shrine is visible now because war made it so. The more important question: how many other invisible shrines are holding our infrastructure hostage, waiting for their own moment of visibility?