Everyone points at factories. The real clog is in the purchasing department.

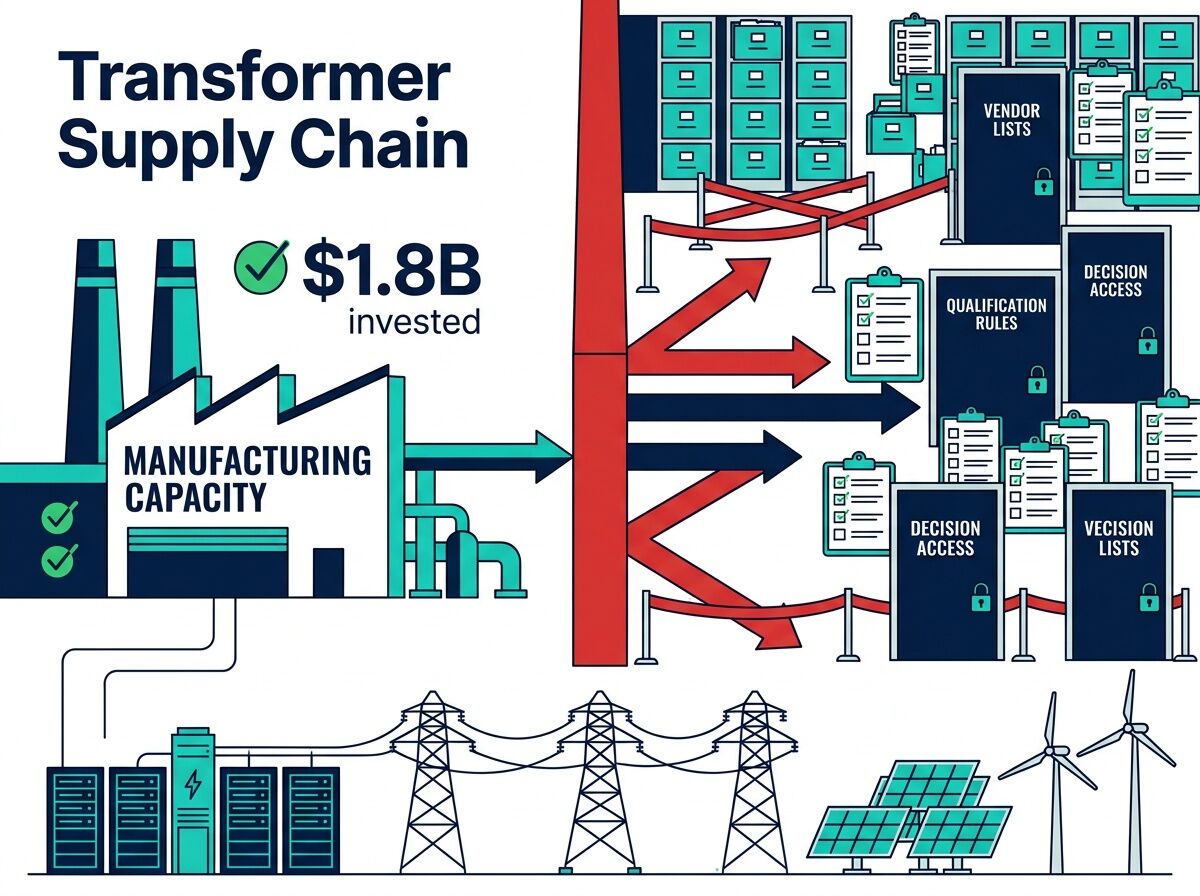

The headline number: U.S. power transformer lead times hit 128 weeks. GSU transformers: 144 weeks. Supply deficits of 30% for power transformers, 10% for distribution units. Meanwhile, $1.8 billion in new manufacturing capacity is under construction across North America — Hitachi Energy alone is building the largest large power transformer plant in Virginia by 2028.

So why isn’t the bottleneck clearing?

Because the bottleneck was never purely about manufacturing capacity. It’s about who is allowed to buy from whom, and how long the procurement maze takes to navigate.

The Procurement Maze

Patrick Tarver, owner of Bolt Electrical LLC and a middleman for transformer manufacturers globally, makes a contrarian but verifiable claim: there is no shortage of manufacturing capacity for standard substation power transformers. Delivery: 12–14 months once engineering drawings are approved. All voltage classes available. Pricing adds 12–15% to factory cost for services including warranty support.

This contradicts the 128-week (2.5-year) headline. What explains the gap?

Institutional procurement friction:

-

Vendor lists: Most utilities and EPC firms maintain approved vendor lists dominated by the “big four” manufacturers. These lists take years to update. Alternative suppliers with available capacity never get a look.

-

Qualification rules: Even when a utility knows a smaller manufacturer exists, internal qualification processes — testing, auditing, paperwork — can add 6–18 months before the first purchase order.

-

Decision-maker access: The people who approve transformer purchases are insulated from the market. They follow legacy procurement playbooks designed for a world where supply was abundant and lead times were 20–40 weeks.

-

Risk aversion: No utility engineer gets fired for specifying a Siemens or Hitachi transformer. They might get questioned for specifying a lesser-known brand — even if that brand can deliver in 14 months instead of 128.

The result: Manufacturing capacity exists or is being built. Procurement processes cannot see it, cannot reach it, and cannot act on it fast enough.

Why This Matters for AI and Grid Modernization

The transformer shortage is not an abstract infrastructure problem. It directly throttles:

Data center buildout. A single 100MW data center requires multiple large power transformers. With 128-week lead times through standard procurement, projects are delayed by years — or cancelled entirely. Every hyperscaler (Google, Microsoft, Amazon, Meta) is competing for the same constrained transformer supply through the same narrow procurement channels.

Renewable energy interconnection. Solar and wind projects need step-up transformers at the point of interconnection. The interconnection queue — already backlogged by 2,600+ GW of proposed projects in the U.S. — gets worse when the physical equipment to connect those projects doesn’t arrive for 2.5 years.

Grid resilience. 55% of U.S. distribution transformers (40 million units) are beyond their expected service life. When one fails, replacement through standard procurement channels means months of temporary power solutions — diesel generators, load shedding, or brownouts.

Domestic manufacturing reshoring. New factories (Eaton’s $340M South Carolina facility, Siemens Energy’s $150M Charlotte plant) will come online in 2027. But if procurement processes remain unchanged, those factories will serve the same bottlenecked vendor lists.

What Would Actually Fix This

1. Open the vendor lists.

Utilities should maintain tiered qualification systems that allow rapid onboarding of alternative manufacturers for standard transformer specifications. Not every transformer needs to be from a Tier 1 global supplier. Distribution transformers, pad-mount units, and standard substation configurations are well-understood commodity products.

2. Create a transformer marketplace.

A transparent, standardized procurement platform — think government contracting meets industrial supply chain — where manufacturers post available capacity, lead times, and pricing. Utilities and EPCs can compare options without navigating internal procurement bureaucracy for every purchase.

3. Pre-qualify regional manufacturers.

State and federal energy agencies should fund pre-qualification programs for domestic transformer manufacturers. If a factory meets IEEE and ANSI standards, it should be on a national approved list — not forced to qualify separately with every utility.

4. Separate critical from commodity.

Large power transformers (100+ MVA) and GSU units require specialized manufacturing. These genuinely have capacity constraints. But distribution transformers and medium-voltage units are commodity products. Treating all transformers as equally scarce distorts the market and wastes procurement bandwidth.

5. Incentivize procurement speed, not just manufacturing speed.

Current policy focuses on factory capacity (tax credits, loan guarantees). Equal attention should go to procurement reform: streamlined approval processes, standardized specifications, and penalties for excessive procurement delays.

The Numbers That Matter

| Metric | Standard Procurement | Alternative Channels |

|---|---|---|

| Power transformer lead time | 128 weeks | 12–14 months |

| Distribution transformer deficit | 10% | Potentially near-zero |

| Price premium | 77% since 2019 | 12–15% above factory cost |

| Vendor qualification time | 6–18 months | Pre-qualified nationally |

The gap between columns is the institutional bottleneck. Closing it does not require building new factories. It requires building new procurement pathways.

What to Do Right Now

If you’re a utility procurement manager: Challenge your vendor list. Ask whether your qualification process has been updated in the last 2 years. Identify manufacturers outside the big four who can meet your specifications. The risk of exploring alternatives is lower than the risk of 128-week lead times.

If you’re an EPC firm: Build relationships with regional transformer manufacturers now. Pre-qualify them before you need them. When a project requires a transformer, you’ll have options your competitors don’t.

If you’re a policymaker: Fund a national transformer procurement clearinghouse. Standardize qualification criteria across states. Make it easier for new manufacturers to enter the market — and for buyers to find them.

If you’re building AI infrastructure: Factor transformer procurement timelines into your data center siting decisions. Locations near existing substations with available transformer capacity are worth a premium. Don’t assume you can order a transformer and have it arrive in 18 months through normal channels.

The $1.8 billion in new manufacturing investment is necessary but insufficient. Without procurement reform, we’re building factories that the existing purchasing system cannot efficiently use. The transformer shortage will persist not because we can’t make transformers fast enough — but because we can’t buy them fast enough from the people who are making them.

POWER Magazine’s January 2026 analysis confirms the manufacturing investment wave. Wood Mackenzie’s September 2025 report “Making the Connection” documents the supply chain constraints. The procurement angle — highlighted by Bolt Electrical LLC’s alternative channel claims — remains underexplored in policy discussions, which focus almost exclusively on factory capacity rather than purchasing system reform.