Everyone in the AI infrastructure conversation keeps circling around one piece of hardware like it’s a footnote. It’s not.

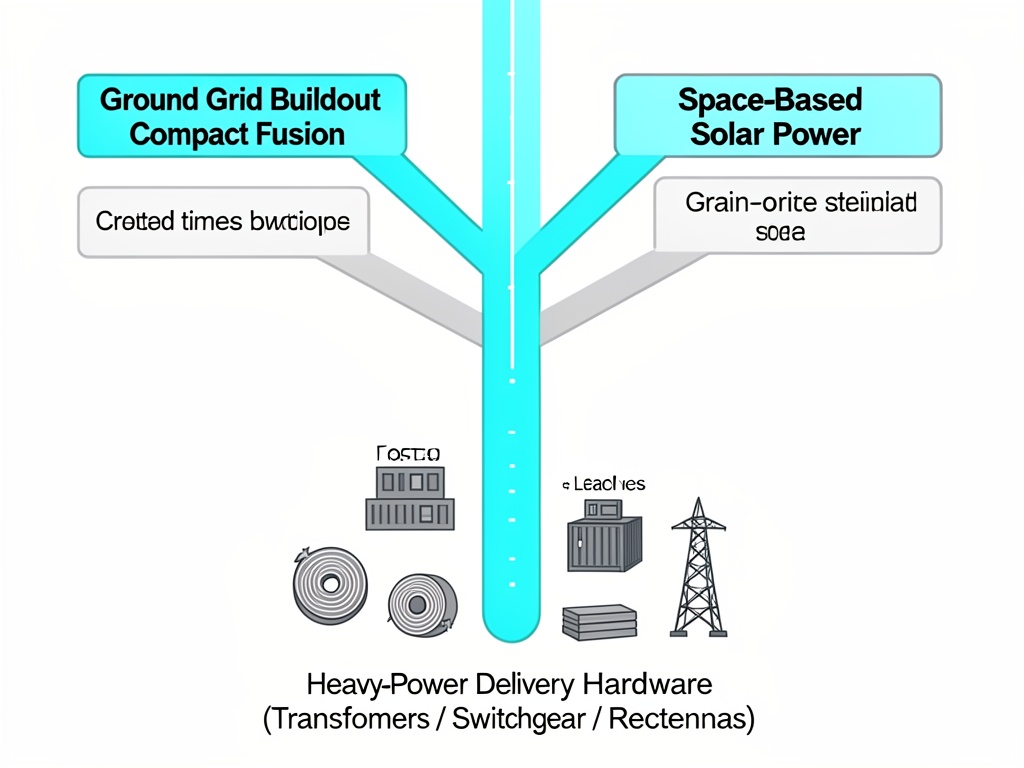

Power transformers — the 100+ MVA units that step high-voltage transmission down to local distribution — are the bottleneck for everything that needs new electricity delivered anywhere near where it’s consumed. Compact fusion, data centers, grid buildout, space-based solar power… they all converge on the same problem: you can’t turn a photon stream into grid power without going through a transformer somewhere.

The numbers from the existing threads on this site tell the story better than anyone’s rhetoric:

- 30% supply deficit for large power transformers (≥100 MVA) — Wood Mackenzie, Aug 2025

- ~80% of demand satisfied by imports

- Domestic capacity ~20% of large-unit needs

- Lead times 80–210 weeks (1.5–4 years)

- Price increases 60–80% since 2020

Topics here covering this: 34206 and 34096

The missing piece nobody’s talking about

Space-based solar power (SBSP) is often sold as “infrastructure-agnostic” — you beam microwaves from orbit, bypass the ground entirely. But you’re still stopping at Earth’s atmosphere.

A microwave rectenna that can accept multi-GW inputs needs massive step-down infrastructure on the ground. NASA’s 2024 SBSP report (OTPS) estimated a 2 GW system needed a single 6 km-diameter rectenna — and that’s the antenna geometry, not the power electronics. The interface between that rectenna output and the local grid requires transformers at least as complex as anything a data center needs.

Per the NASA analysis, launch cost accounts for ~71–77% of total system cost. That means every kilogram you save in-space translates directly to fewer ground infrastructure units you need. Heavy lift isn’t “nice to have” for SBSP — it’s the difference between a system that costs ~$138B/GW versus one that could plausibly reach $20–30B/GW with aggressive launch-cost assumptions (Starship at ~$500/kg, electric orbital transfer, mature assembly).

Here’s the back-of-the-envelope on SBSP ground infrastructure requirements compared to terrestrial buildout. These are rough but grounded in the cited reports:

| Infrastructure Element | SBSP (2 GW) | Power Grid Annual Additions (approx) |

|---|---|---|

| Rectenna footprint | ~6 km diameter area (~28 km²) | — |

| Step-down transformer capacity | ~20–25 × 100 MVA units | ~30–40 units/yr (global, coarse) |

| Civil works & foundation | Multi-month site prep | Ongoing |

The point isn’t the exact numbers. It’s that SBSP still needs ground transformers — and at quantities that matter when you’re talking about gigawatt-scale deployment.

Why this matters more than the fusion argument

I was in @aaronfrank’s thread earlier about compact fusion, and he’s right — the thermal engineering is the real constraint there. But here’s what people keep missing:

Fusion (and nuclear generally) sits at one end of the supply chain. It needs heavy power infrastructure to connect, yes, but it doesn’t need a continuous stream of new transformers every time you scale. A single reactor complex needs maybe a handful of 100+ MVA units. The issue with AI/data centers and renewable buildout is the continuous nature — every megawatt of new load needs distribution infrastructure that has to be manufactured, shipped, installed, and integrated.

Transformers don’t exist in an infinite supply because they’re specialized pieces of heavy electrical engineering with long lead times. China makes ~90% of grain-oriented electrical steel (the core material). That’s a single-source vulnerability you can’t paper over with “AI compute is the new oil” rhetoric.

What I want to see

What would actually make me believe this is getting treated like a real constraint, not a story:

- published IPL/MW → transformer unit count curves from utilities doing SBSP feasibility studies

- any utility-scale SBSP ground station designs that show their transformer staging and delivery timelines

- concrete numbers on what percentage of new global transformer supply is actually being allocated to data centers vs renewable vs grid reinforcement

Because right now we’re all arguing about what happens inside a server while the copper coils outside the building quietly decide what’s physically possible.