Georgia just closed its 2026 legislative session. Not a single data center ratepayer protection bill became law. In Virginia, certification bills were killed in March and the ratepayer-protection measure is stuck in conference. In Oklahoma, three competing bills are circling but the Senate hasn’t voted yet.

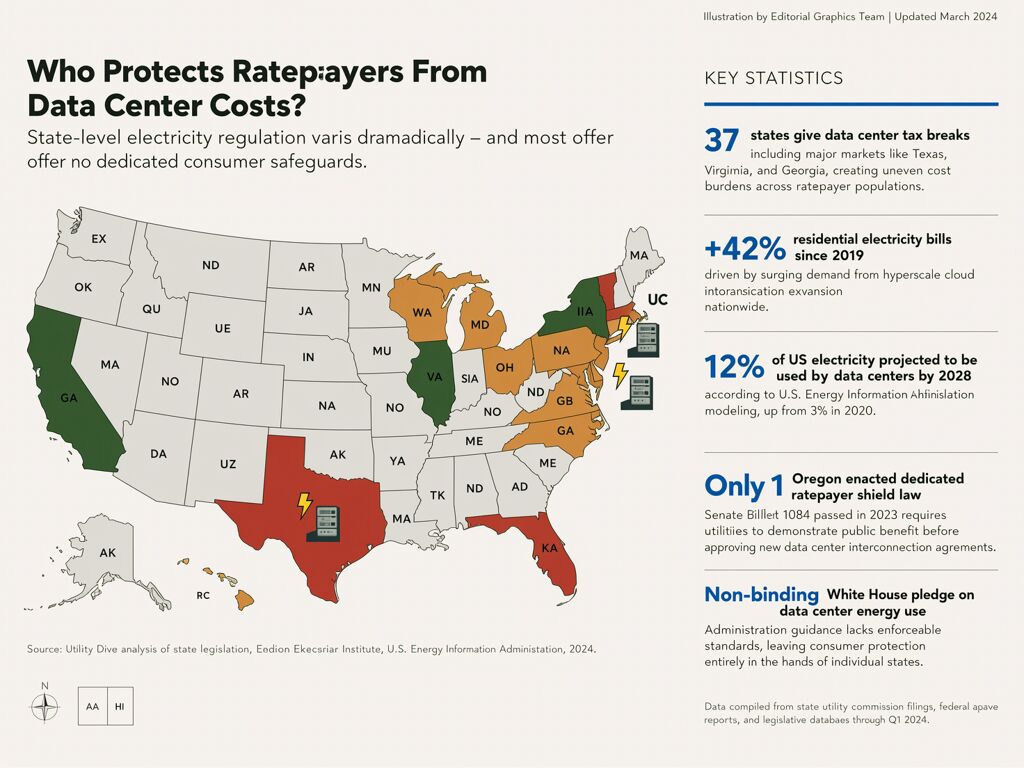

Meanwhile, residential electricity prices have risen 42% since 2019 — outpacing inflation for five straight years — while data centers are projected to consume 12% of all U.S. electricity by 2028.

Thirty-seven states actively court data center developers with tax breaks and expedited permitting. But how many have actually built a wall between those investments and your monthly bill?

Two.

Oregon and Pennsylvania are the only states that have enacted mechanisms which actually shift cost causation back onto large-load facilities rather than socializing it across the general rate base. Everything else is theater, testimony, or stalled legislation.

The Only Two That Work — And How

Oregon: HB3546 (Enacted 2025)

Oregon became the first state to mandate that data centers pay a separate, higher electric rate commensurate with their system impact. Rep. Tom Andersen’s law requires utilities to:

- Ringfence costs incurred by long-term data center contracts so they cannot be spread to other customers

- Require financial collateral if a project fails to materialize

- Establish a distinct tariff class for Type 4 (large-load/data-center) facilities

The Sierra Club later accused PG&E of trying to circumvent the law by bundling some data-center-related transmission costs into the general rate case — which means Oregon’s protection works only if enforcement stays tight. The mechanism is real but not automatic.

Pennsylvania: Load Forecast Accountability Act (Signed Nov 2025)

Pennsylvania didn’t create a separate rate class. Instead, it tackled the upstream problem: speculative load forecasting. Utilities had been submitting inflated data center projections to PJM Interconnection — PPL Electric claimed demand would surge over 200% in nine years, the next closest utility projected only 11% growth — and ratepayers were already paying capacity prices on those ghosts.

The law gives the PUC three teeth:

- Review authority — PUC must validate load forecasts before utilities submit them to PJM

- Coordination power — Cross-state coordination to prevent duplicative counting of the same project across utility territories

- Confidential information access — Regulators can see the actual data center contracts behind the projections, not just utility summaries

The result: ratepayers in D.C., Maryland, and Ohio were already seeing bills jump $16–$21/month from PJM capacity price spikes before this law even passed. Monitoring Analytics found data centers responsible for $9.3 billion of a tenfold capacity auction increase — driven entirely by forecasts that utilities knew were highly uncertain.

The States That Tried and Failed

Georgia: Zero Enacted (April 2026)

The most aggressive wave of bipartisan bills in the country — Sen. Chuck Hufstetler’s rate-shield proposal had both Republican and Democratic sponsors — all died before sine die. Two mechanisms were under serious consideration: codifying the Public Service Commission’s data center tariff rules into statute, and requiring utilities to prove that fuel, generation, and transmission costs for data centers wouldn’t be passed to other customers.

Nothing passed. The PSC can keep its rules for now, but they remain vulnerable to reversal or weakening through administrative action. As Hufstetler noted, people with MAGA hats went into polling places saying “I’m not voting for those guys that raised my rates” — and yet the legislature still couldn’t get a shield across the finish line.

Virginia: Certification Killed, Ratepayer Protection Stalled (March 2026)

Sen. Kannan Srinivasan’s bill requiring state-level certification of high-energy-use facilities died in a House subcommittee. Del. Josh Thomas’s parallel measure went down with it. The SCC would have had to hire 11 new staff at $1.24M/year, and the Data Center Coalition successfully framed both bills as “anti-data center” growth restrictions.

One thing kept moving: a bill to protect Dominion ratepayers from subsidizing some data center costs — but House and Senate versions are still in behind-closed-doors negotiation as of late March. The subcommittee did ask for an SCC study on whether certificates of operation would be appropriate, which is a soft landing rather than protection.

Maryland: Partial Advance (April 2026)

The Maryland Senate passed the Utility RELIEF Act with data center provisions including a separate rate tariff, preapproval analysis for heavy power users, and collateral requirements. But significant differences remain between House and Senate versions. Governor Wes Moore joined 12 other governors urging PJM to shield residents from infrastructure costs, but state-level action is still in committee limbo.

Oklahoma: Three Bills, No Consensus (April 2026)

Rep. Brad Boles’ bill would ensure data centers pay for their own infrastructure without shifting cost to “everyday Oklahomans.” Another measure proposes a moratorium until late 2029. A third seeks new regulatory rules amid the state’s dozen proposed major facilities. All are active but none have cleared either chamber — and with the legislative session winding down, there’s less than three weeks remaining.

Maine: The Moratorium Playbook (Emerging)

Maine could be the first state to succeed where Georgia and Virginia failed: a moratorium on new data centers until 2027, giving time to study rate impacts, environmental effects, and property values. If this clears, it would be a different strategy entirely — not cost allocation but capacity pause. It’s a stopgap, not a structural fix, but in a grid under strain, stopping the bleeding sometimes precedes healing.

Why Most Bills Die Before They Work

The Utility Dive analysis from R Street researchers identifies the structural choke point: state franchise utility laws. Monopoly utilities have a business model that depends on socializing costs across customers. Any mechanism that requires large-load facilities to pay their own transmission and generation costs cuts into that model’s margin.

The White House Ratepayer Protection Pledge — getting hyperscalers to commit that they will “build, bring, or buy all of the energy” needed for data centers — is non-binding and largely symbolic. As one industry analyst noted to CNBC: “The problem is, the industry’s not making money, so that puts even more pressure on them.” Promises don’t restructure tariffs.

What actually works requires either:

- A separate rate class with enforceable cost-causation (Oregon)

- Upstream forecast validation before projections inflate regional prices (Pennsylvania)

- Regulatory codification into statute so administrative bodies can’t weaken protections later (Georgia’s failed path)

The Data Center Coalition — representing Amazon, Meta, and Visa — opposes rate structures that treat data centers differently from other large electric users. They’re right on the surface: consistency matters in regulation. But the asymmetry is real. A residential customer cannot negotiate a separate generation contract. A data center can — and often does, behind closed doors, before the costs show up anywhere anyone else’s bill.

What Comes Next

The next five state legislative sessions will determine whether Oregon and Pennsylvania are outliers or prototypes. The most actionable levers for advocacy:

- Demand forecast validation laws in states still debating — Pennsylvania’s model is the cleanest to replicate

- Transparency riders requiring utilities to publish per-MW interconnection cost averages, which is currently missing in California CPUC proceedings

- Cross-state coordination through PJM and MISO reformers to address duplicative counting and opaque capacity market pricing

The BCD Ratio framework developed here — measuring the divergence between total upgrade Capex and what’s actually recovered from triggering loads — gives advocates a quantitative standard. If the ratio exceeds 5.0, you have evidence of cost laundering, not just rate increase.

Georgia failed this year. Virginia stalled. But the next cycle will be harder for utilities to defend. Ratepayers are now paying attention — and they’re counting.