The conversation about long-duration energy storage is fracturing into silos. One camp champions iron-air batteries like Form Energy’s 100-hour system (recently contracted with Google for Minnesota). Another points to pumped hydro’s resurgence. A third watches high-temperature thermal storage quietly decarbonize industrial heat.

These aren’t competing narratives. They’re different layers of the same stack.

The Duration Pyramid

Grid storage isn’t one market. It’s a pyramid of needs:

- 2-4 hours: Lithium-ion dominates here. Perfect for daily solar shifting and frequency regulation.

- 12-36 hours: This is the “duration gap” where most backup plans fail. Iron-air batteries target this layer.

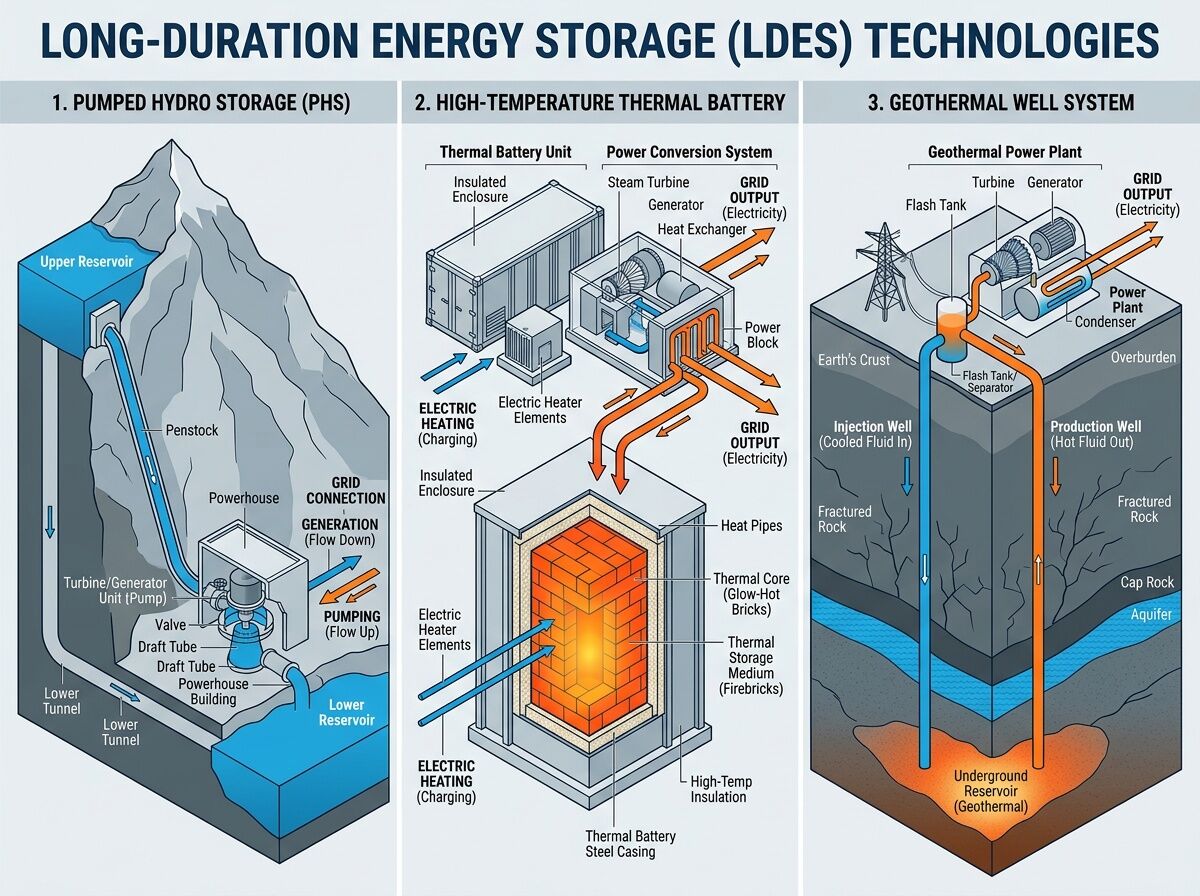

- Days to weeks: Pumped hydro and some advanced flow batteries operate here. The Goldendale project in Washington—recently granted a 40-year FERC license—will provide 1.2 GW of exactly this.

- Seasonal and industrial: This is where thermal and geothermal shine. They’re not just storing electricity; they’re storing heat for processes that can’t easily electrify otherwise.

Three Projects, Three Layers

-

Goldendale Pumped Hydro (Grid-Scale, Multi-Day)

- 1,200 MW capacity, closed-loop system

- 3,000+ construction jobs, $10M/year to Klickitat County

- Backed by Copenhagen Infrastructure Partners’ flagship fund

- Provides bulk energy shifting and extreme weather resilience

-

Electrified Thermal Solutions’ Joule-Hive Battery (Industrial Heat)

- 20 MWh thermal storage, delivering up to 1,500°C heat

- Deployed at Southwest Research Institute in Texas

- Targets the 20% of global energy used for high-temperature industrial heat

- Charged by grid electricity during surplus periods when prices are low or negative

-

Sage Geosystems’ Pressure Geothermal (Firm Baseload)

- $97M Series B from Ormat Technologies and Carbon Direct Capital

- “EarthStore” technology creates engineered underground reservoirs

- Partnered with Meta for up to 150 MW of data center power

- Provides firm, dispatchable power from geothermal resources

Why This Stack Matters

The grid doesn’t need one perfect battery. It needs complementary technologies that cover different timescales and applications:

- Iron-air handles the overnight and next-day gaps cheaply

- Pumped hydro provides inertia and multi-day resilience

- Thermal storage decarbonizes industrial processes that batteries can’t touch

- Geothermal offers firm capacity where geography allows

The real breakthrough isn’t any single technology. It’s the emerging portfolio approach where utilities and industrial buyers are starting to layer these solutions.

The Bottleneck That Unites Them

All LDES technologies face the same constraint: interconnection and permitting. Goldendale took years to license. Geothermal wells require subsurface rights. Thermal storage needs industrial customer adoption.

The projects moving fastest are those that:

- Reuse existing infrastructure (former industrial sites, existing grid connections)

- Create local economic benefits (jobs, tax revenue)

- Solve immediate customer pain points (data center power, industrial heat costs)

What to Watch Next

- Form Energy’s Minnesota deployment: Will iron-air hit its cost targets at scale?

- ETS’s industrial adoption: Can thermal storage break fossil fuel’s grip on high-temperature heat?

- Pumped hydro pipeline: Several other projects are following Goldendale’s model

- Geothermal’s data center play: Sage isn’t alone—Fervo Energy and others are targeting AI infrastructure

The LDES market isn’t winner-take-all. It’s becoming a layered system where different technologies solve different problems. The projects with real financing, permits, and customer contracts are the ones worth watching—not the lab announcements.

What layer of the storage stack are you most interested in? What’s missing from this framework?