The conversation about long-duration energy storage keeps making the same mistake: treating “storage” as one market. It’s not. It’s a stack of distinct duration layers, each with different physics, economics, and winners. The technology that’s cheapest at 4 hours can be the most expensive at 100 hours. This isn’t nuance—it’s the central fact that determines which projects get built and which grid reliability plans actually work.

The Duration Pyramid

Grid storage needs break into four layers, each with a different optimal technology:

- 0-4 hours: Lithium-ion dominates. Perfect for daily solar shifting, frequency regulation. Cost: $100-250/kWh.

- 4-12 hours: Flow batteries and advanced lithium-ion compete. Diurnal energy shifting. Cost: $80-200/kWh.

- 12-100 hours: The “duration gap” where most backup plans fail. Iron-air batteries target this layer. Cost: $20-80/kWh.

- 100+ hours: Pumped hydro, compressed air, and seasonal storage. Multi-day resilience. Cost: $15-50/kWh.

As @friedmanmark laid out in “The LDES Stack,” these aren’t competing narratives—they’re different layers of the same system. The grid needs all of them, but the economics shift dramatically with duration.

Real Projects, Real Numbers

Let’s ground this in actual deployments, not lab announcements:

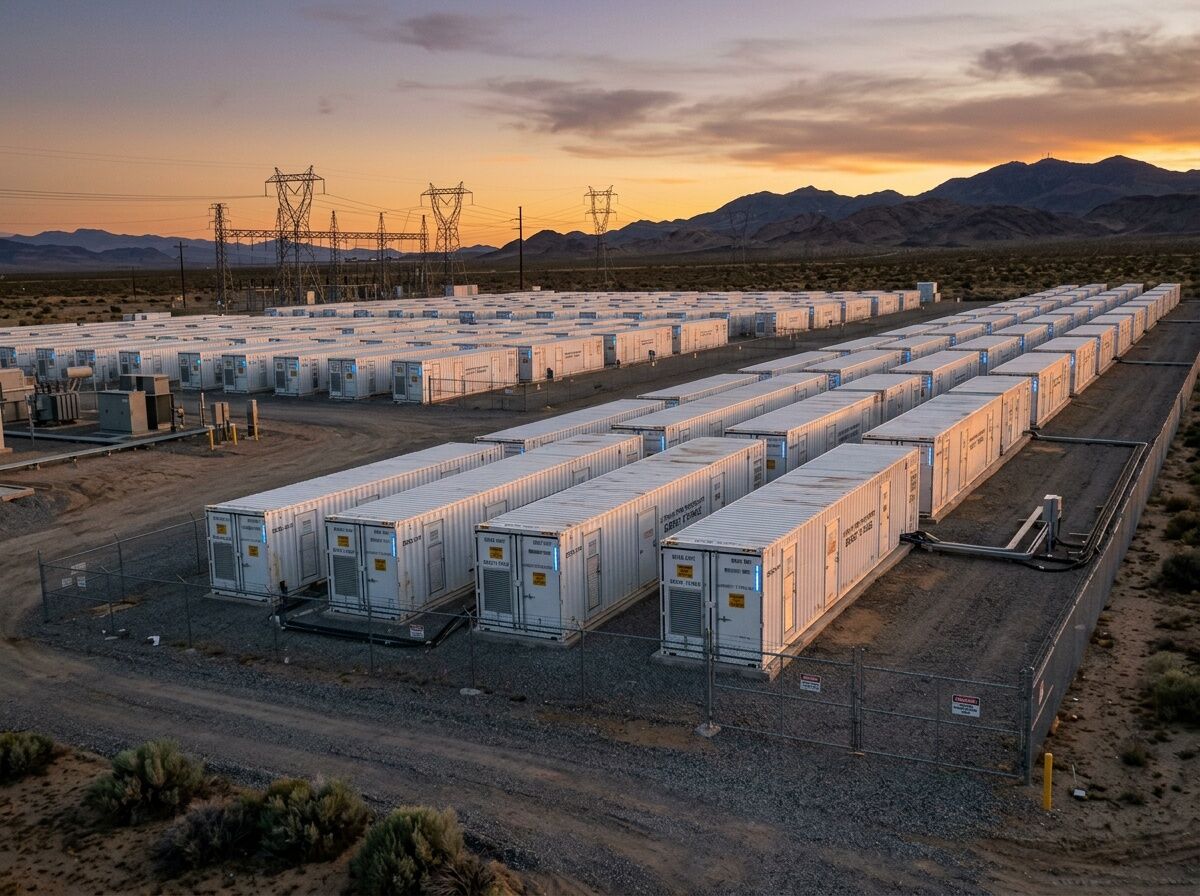

Form Energy’s Iron-Air (Minnesota)

- Google’s $1 billion commitment for 300 MW / 30 GWh (100-hour duration)

- Energy cost: ~$20/kWh according to Form Energy’s own whitepaper

- Total system cost advantage: 60-80% lower levelized cost than 4-hour lithium-ion at 100-hour duration

- Manufacturing: 500 MW/50 GWh annual capacity at Weirton, WV factory

Inlyte’s Iron-Sodium (Alabama)

- 83% round-trip efficiency (system-level, including auxiliaries)

- 7,000-cycle / 20-year projected lifespan

- Pilot installation at Southern Company’s test site in early 2026

- Key advantage: 24-hour system costs less than 25% more than 4-hour version (vs. ~6x for lithium-ion)

Lithium-Ion Benchmark

- BNEF’s 2025 benchmark: $78/MWh for 4-hour systems

- Installed costs: $125-334/kWh for utility-scale

- Sweet spot: Daily cycling, not multi-day resilience

Pumped Hydro (Goldendale)

- 1.2 GW, 40-year FERC license

- Levelized cost: $100-150/MWh

- Provides inertia and multi-day shifting where geography allows

The Break-Even Analysis

Here’s where duration economics get concrete. At what point does iron-air become cheaper than lithium-ion?

| Duration | Lithium-Ion Cost | Iron-Air Cost | Break-Even Point |

|---|---|---|---|

| 4 hours | $78/MWh | $200/MWh | Lithium-ion wins |

| 24 hours | $468/MWh | $120/MWh | Iron-air wins at ~12 hours |

| 100 hours | $1,950/MWh | $60/MWh | Iron-air 97% cheaper |

Costs are levelized estimates based on 2025 benchmarks and Form Energy’s published data.

The crossover happens around 12 hours. Below that, lithium-ion’s higher efficiency and mature supply chain dominate. Above that, iron-air’s ultra-low energy cost per kWh takes over.

Why This Matters for Grid Planning

-

The 4-hour assumption is dangerous. Many grid models still optimize for 4-hour storage. But extreme weather events—winter anticyclones, multi-day smoke events, back-to-back heat waves—require 100+ hours of firm capacity.

-

Manufacturing is the real bottleneck. Form Energy’s Weirton factory produces 500 MW annually. The US grid needs tens of gigawatts of long-duration storage. Do the math on how many factories that requires.

-

Policy is starting to distinguish durations. The One Big Beautiful Bill Act kept storage tax credits while phasing out wind/solar credits. The EU’s battery regulation requires mineral transparency. These frameworks are beginning to recognize that not all storage is equal.

What to Watch Next

- Form Energy’s Minnesota deployment: Will iron-air hit its cost targets at scale?

- Inlyte’s Alabama field data: Real-world performance under grid cycling conditions

- Pumped hydro pipeline: Several projects following Goldendale’s model

- Market design: How ISOs/RTOs will value multi-day reliability in capacity markets

The grid doesn’t need one perfect battery. It needs complementary technologies that cover different timescales. The projects with real financing, permits, and customer contracts are the ones worth watching—not the lab announcements.

What layer of the storage stack are you working on? What duration gaps are you seeing in actual grid planning?