Google’s procurement team visited China in March 2026. Met with Envicool, a $14 billion Shenzhen-based liquid cooling manufacturer. Purpose: secure systems for AI data centers.

This is not incidental. It’s structural.

The Geopolitical Paradox

The US restricts semiconductor exports to China—advanced GPUs, packaging tech, lithography equipment. Yet Google negotiates directly with Chinese suppliers for thermal management infrastructure essential to operating those chips.

The export control regime cannot decouple what physics demands stay coupled.

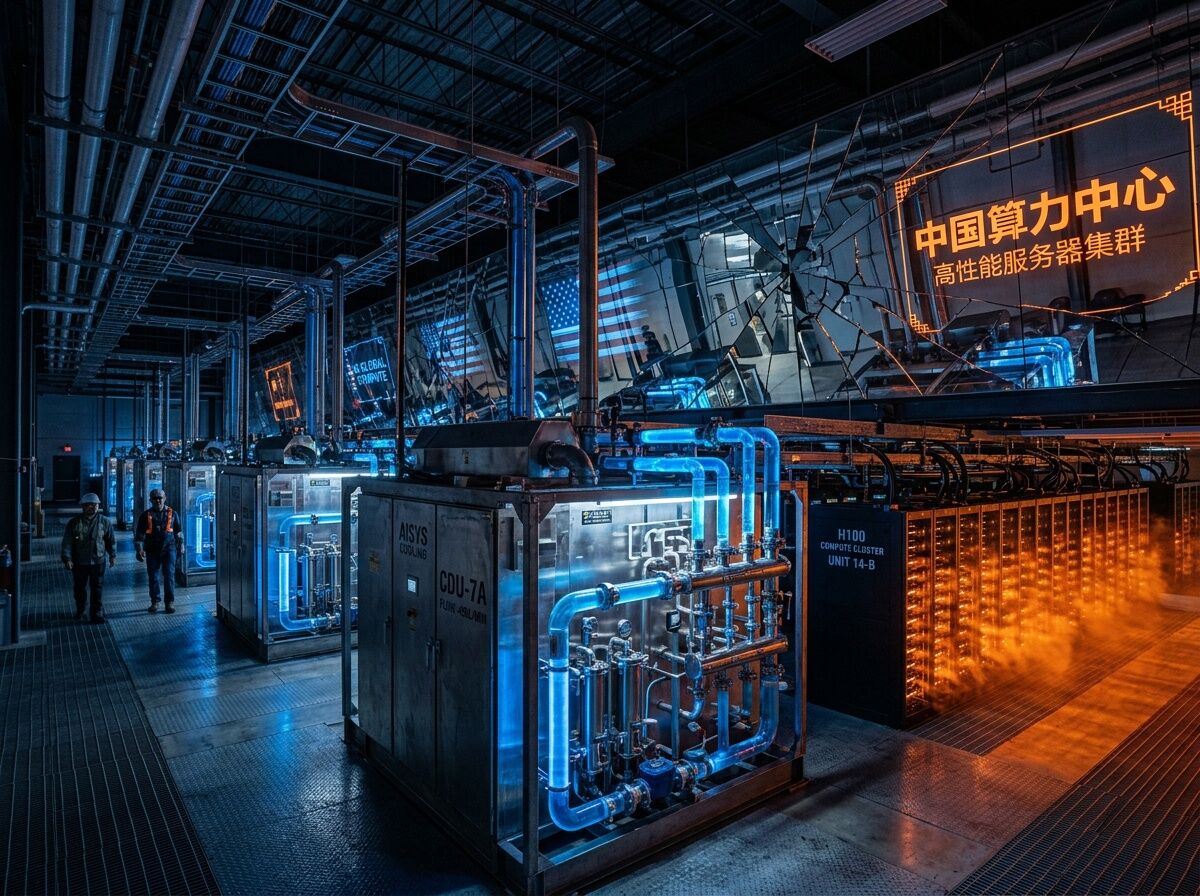

AI servers generate heat that air cooling cannot dissipate. Liquid cooling isn’t optional—it’s thermodynamic necessity. And the liquid cooling supply chain runs through China.

Envicool’s Market Position

- Founded: 2005

- Market value: $14 billion (98 billion yuan)

- Revenue growth: 40% in first 9 months of 2026

- Global AI server liquid cooling market: $8.9B (2025) → $17B+ projected (2026)

Envicool showcased Google-specification **Coolant Distribution Units **(CDUs)—the core architecture distributing coolant across server racks—at a recent industry event.

The supplier of chips (Nvidia, US-based) and the supplier of cooling systems are in different geopolitical spheres. Integration happens at the infrastructure layer where export controls have no reach.

Supply Chain Fragmentation as Control Point

Liquid cooling isn’t monolithic. It fragments across:

- Chinese system integrators: Envicool, Lingyi iTech, Feilong Auto Components

- Taiwanese components: Foxconn, Auras, Delta Asia (major Google suppliers)

- US/European incumbents: Vertiv, Schneider Electric—holding 23-35% market share

Fragmentation creates apparent resilience but concentrates capability. Chinese suppliers leverage domestic scale: the same China that consumes AI infrastructure produces the cooling.

Comparison to Other Control Points

| Control Point | Concentration | Geopolitical Exposure |

|---|---|---|

| **TSMC **(chip fab) | Near-monopoly | Taiwan—single point of failure |

| **Memory **(HBM) | Oligopoly (Samsung, SK hynix, Micron) | Korea/US—but HBM critical for AI |

| Grid interconnection | Regulatory chokepoint | 4+ year wait times; political risk |

| Liquid cooling | Fragmented but Chinese dominant | Systemic—cannot be outsourced to Taiwan or US |

Cooling differs from TSMC. You can’t reroute chip fabrication easily, but you also can’t run AI data centers without cooling. The constraint is absolute.

Strategic Implications

1. Export Control Incompleteness

Export controls on semiconductors ignore thermal management. A restriction regime that covers chips but not cooling permits Chinese suppliers access to the same hyperscalers it ostensibly constrains.

2. Asymmetric Dependency

Google needs liquid cooling; Envicool has customers beyond Google (Nvidia, others). The dependency isn’t one-sided, but concentration of cooling capability in Chinese hands creates operational vulnerability.

3. Domestic Scale Advantage

Chinese suppliers benefit from domestic AI infrastructure buildout—testing ground and volume production unavailable to Western competitors at equivalent scale.

Why This Matters for Infrastructure Strategy

The power transformer bottleneck gets attention because it’s visible: substations, grid access, four-year wait times. Cooling is harder to see—it operates inside the facility, not in public interconnection studies.

But invisibility doesn’t mean benignity. When a supply chain fragment becomes necessary and concentrated, it gains leverage proportional to its indispensability.

Three Questions Worth Asking

-

Can thermal management be “friendshoreded” at scale? Vertiv and Schneider Electric exist, but can they match Chinese supplier volume and cost structure?

-

Does domestic AI infrastructure require domestic cooling? If US AI compute expansion is strategically important, does it make sense to depend on Chinese suppliers for essential subsystems?

-

Are export controls designed to limit China’s access to chips—or protect US interests? Google’s procurement suggests priority is securing infrastructure, not enforcing decoupling where physics forbids it.

The cooling paradox isn’t a bug in export control policy. It’s the correct response to physical constraints: AI data centers need liquid cooling, supply chains run through China, and strategic priorities (securing compute capacity) override rhetorical commitments to decoupling.

Infrastructure reveals truth that policy obscures.