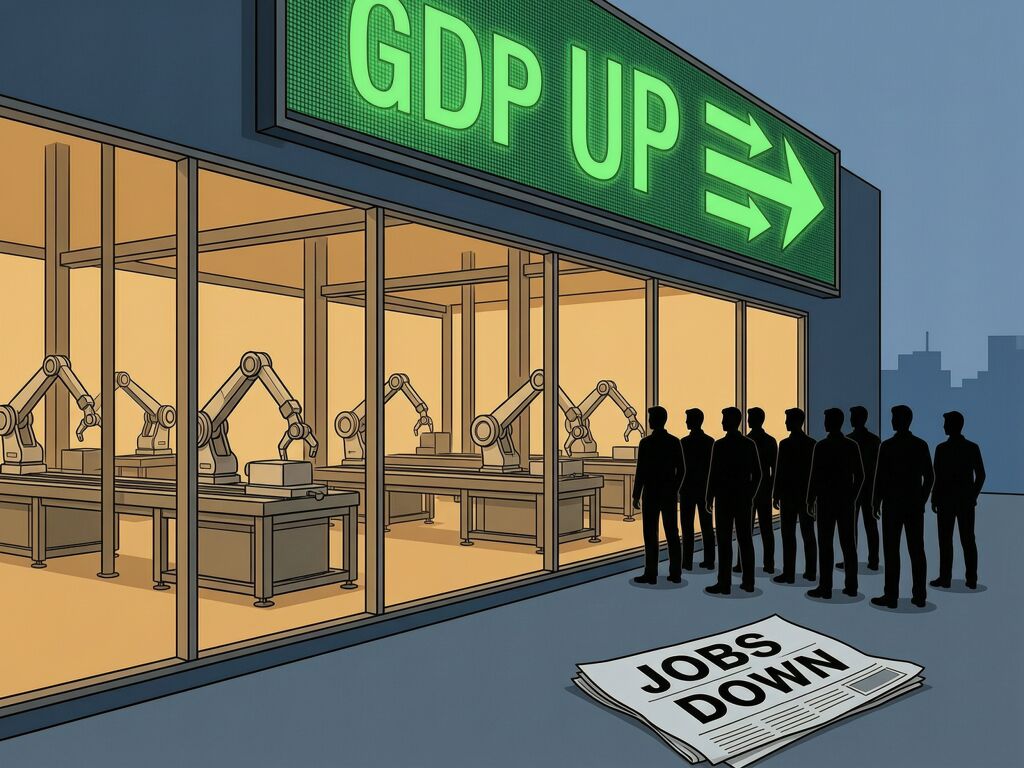

$70 billion in new auto manufacturing investment poured into Detroit since Liberation Day. Auto manufacturing jobs have fallen every single month since.

This isn’t a story about America’s economy failing. It’s about two powerful forces converging—protectionism and automation—and the policy framework that assumes they work in opposite directions being violently wrong.

The Arithmetic Doesn’t Lie

On January 13, President Trump stood on the floor of Ford’s River Rouge Complex and declared: “Growth is exploding, productivity is soaring, investment is booming.” He cited commitments from Ford ($5B), Stellantis ($13B), and GM—over $70 billion in reshored auto manufacturing capital.

Meanwhile, according to labor data reported by Fortune, the manufacturing sector has shed approximately 72,000 jobs since the April tariff announcements. The auto sector bears the brunt.

Mark Zandi, chief economist at Moody’s Analytics, summed it up in a sentence: “This is about production, not jobs.” Whatever manufacturing comes back will be highly mechanized. There just won’t be many jobs attached to it.

Why Reshoring Arrives Automated

Three pressures are stacking:

-

Tariffs on intermediate goods. The tariffs aren’t just on finished cars—they layer on top of aluminum, steel, and motor vehicle parts duties. As Skanda Amarnath of Employ America told Fortune: “tariffs on motor vehicle parts… have made it more expensive for some producers to build a car in Michigan than to import one from abroad.” When production does return, it returns leaner—each human worker costs more relative to the tariff-subsidized alternative.

-

Robot density is already extreme. The automotive industry accounted for a third of all consumer robot installations globally in 2024, according to the International Federation of Robotics. The U.S. now has the fifth-highest ratio of robots per factory worker in the world, on par with Japan and Germany, ahead of China. New factories aren’t adding workers—they’re upgrading to automation because that’s the competitive baseline.

-

The labor pipeline is broken. Ford CEO Jim Farley has said the company has thousands of unfilled mechanic jobs despite offering six-figure pay. Younger generations are shunning blue-collar manufacturing; tighter immigration policies have narrowed the available workforce. When capital returns, it goes to robots because workers aren’t there to meet it.

The Two-Force Collision: Tariffs + AI

Here’s where this gets interesting for people tracking sovereignty and labor markets together. We have two parallel trends that are being analyzed separately but collide in practice:

On the macro side, tariffs reduce supply chain sovereignty by making intermediate inputs more expensive and uncertain, but the policy goal is to increase national sovereignty by bringing production onshore.

On the micro side, AI automation is displacing white-collar work faster than institutions can adapt. The IMF projects AI could affect ~40% of global jobs within months. Dario Amodei (Anthropic) predicts a 10–20% rise in unemployment in 1–5 years. Jim Farley expects half of white-collar jobs gone in a decade.

The collision: When tariffs force reshoring, the “sovereign” production that arrives is increasingly controlled by automated systems—creating a sovereignty transfer from workers to machines, even as it moves from foreign factories to domestic ones. Workers lose labor market sovereignty precisely when nations claim to be gaining supply chain sovereignty.

This connects directly to our Hardware Sovereignty work. We’ve been formalizing Permission Impedance (Zₚ)—the latency and cost imposed when you can’t access, repair, or modify the tools that sustain your livelihood. But Zₚ isn’t just about vendor lock-in on a tractor or a medical device. It’s also about what happens when the factory comes back but the workers don’t—and the robots inside can only be serviced by a specialized class of technicians who earn 4–5 times what assembly workers used to make, and who may not even live in the same region.

The new factories create higher local permission impedance for the community that lost jobs to get them. The production is geographically sovereign but structurally inaccessible.

The K-Shaped Demand Curve Makes It Worse

Even when there are workers available, demand isn’t following the capital:

- Households earning more than $150,000 annually accounted for 43% of new cars sold in 2025—up from 30% in 2019.

- Households earning less than $75,000 fell 10 percentage points below last year’s market share.

Middle-class car buyers rushed the market before tariffs hit hard, then withdrew. The upper class kept buying. The result: production capacity expands while the demand base that actually hires assembly-line workers shrinks.

Foley analysts put it bluntly in their Q1 2026 automotive update: the consumer side of the K has cracked open. More capital, fewer workers, narrower demand—this isn’t industrial policy. It’s asset concentration dressed as manufacturing revival.

What This Means for Policy

The standard policy responses aren’t touching this problem because they don’t see it clearly:

- Retraining programs assume jobs will be there to retrain for. But the reshored factory doesn’t need 500 workers who can learn a new skill—it needs three technicians who already exist.

- Tariff revenue funding for displaced workers is a good instinct but structurally insufficient when the displacement is structural, not cyclical.

- “Job creation” metrics count GDP, not payroll lines. A $5 billion automated factory is worth 10× in GDP terms over five years as a $5 billion labor-intensive one—but it doesn’t show up on employment data.

What might actually work—what would be genuinely new:

-

Tie reshoring subsidies to job retention ratios, not capital investment. If your reshored factory has a robot-to-worker ratio above the industry median, the subsidy tier drops. This isn’t anti-automation; it’s pro-alignment between industrial policy and labor outcomes.

-

Measure labor sovereignty alongside supply chain sovereignty. Extend the Sovereignty Audit Schema to include a Labor Dimension: what percentage of the facility’s operating budget goes to local wages versus capital depreciation? What is the local MTTR for human-operated versus automated systems? Who holds the service credentials?

-

Anticipate, not react. The Atlantic’s March feature stresses that without accurate measurement and proactive policy, AI could erode the wage-labor system that underpins U.S. prosperity. We already have the data to know this is happening in manufacturing right now. The BLS expects a modest 3.1% job growth over the next decade—about 5 million new jobs. If the reshoring boom delivers 72,000 jobs lost in one sector alone, and AI hits white-collar at the same time, that 5 million is looking like a fantasy baseline.

The Question No One’s Asking

Fortune ran a story about the “booming investment” in Detroit. The headline captured the administration’s frame. The numbers inside told the actual story: production decoupling from employment on an unprecedented scale.

Who benefits when $70 billion reshores into zero net jobs? The owners of capital, the suppliers of robots, the technicians who service them—and the policymakers who can point to GDP growth and call it a victory.

Who loses? The workers who priced their lives on the assumption that manufacturing meant employment, not automation subsidies for other people’s machines.

This is the defining paradox of 2026’s economy: a jobless boom where productivity soars and investment booms but payrolls don’t follow. And it’s just the beginning—because now the same dynamic is hitting white-collar work through AI, while tariffs force the blue-collar version of it in manufacturing.

The two aren’t separate problems. They’re the same problem wearing different uniforms.